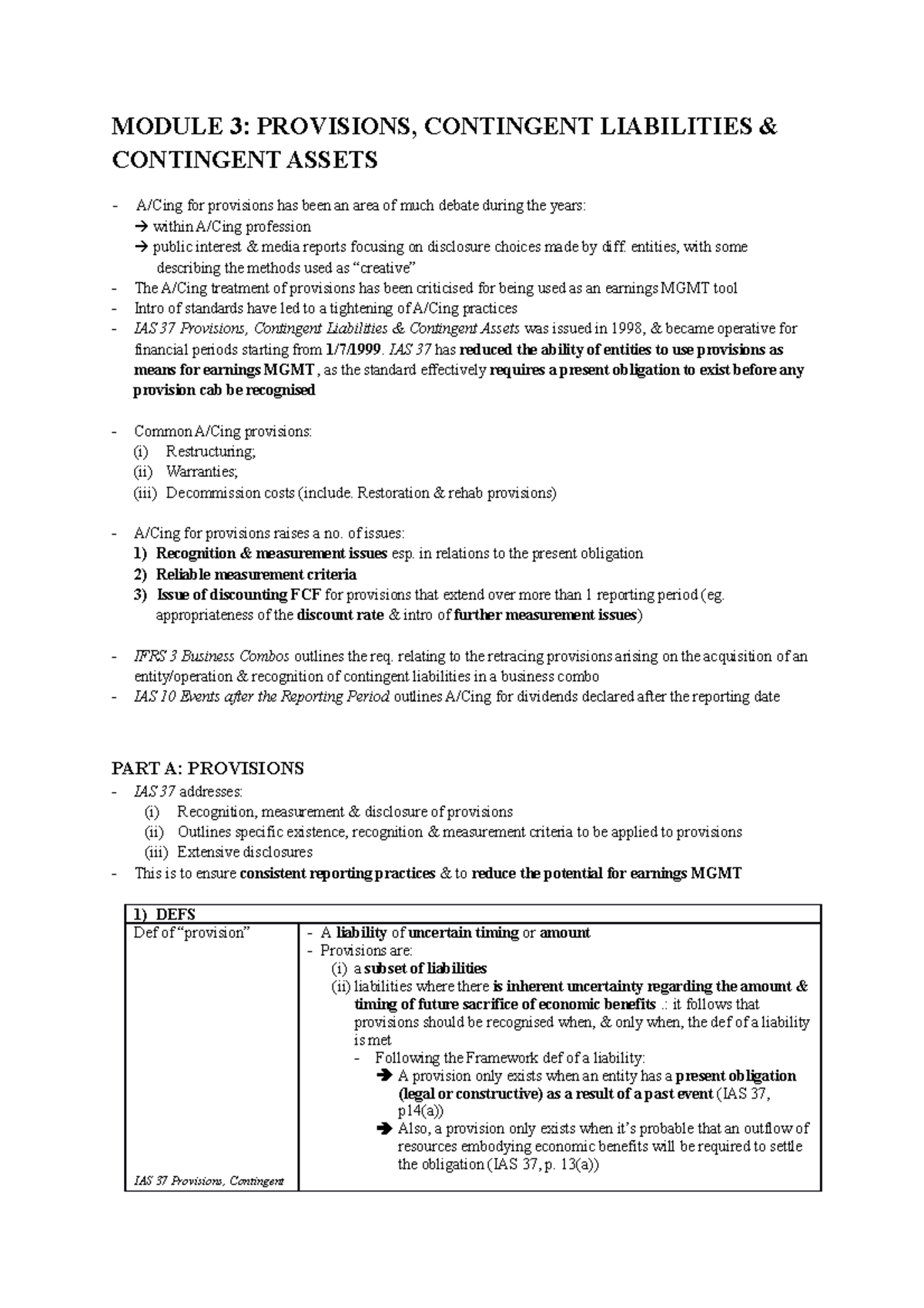

Review Of Provisions, Contingent Liabilities And Assets

Di: Jacob

An entity should disclose a contingent liability, unless the possibility of an outflow of resources embodying economic benefits is remote. A free ‚Basic‘ registration will give .

IAS 37 Provisions, Contingent Liabilities and Contingent Assets Illustrative Examples. Similarly as with contingent liabilities, you should not book anything in relation to contingent assets, but you make appropriate disclosures. A contingent asset is a possible asset arising from past events that will be confirmed by some future events not fully under the entity’s control. AASB 137 is to be read in the context of other Australian Accounting .Provisions, Contingent Liabilities and Contingent Assets.Provisions, contingent liabilities and contingent assets .

IAS 37 — Provisions, Contingent Liabilities and Contingent Assets

The standard prescribes rules regarding the recognition and measurement of provisions, contingent liabilities and contingent assets and also mandates disclosures in .IAS 37 Provisions, Contingent Liabilities and Contingent Assets outlines the accounting for provisions (liabilities of uncertain timing or amount), together with contingent assets .ReMeaSureMent of provisions [IAS 37.This Standard sets out the required accounting treatment and disclosures for provisions, contingent liabilities and contingent assets.Australian Accounting Standard AASB 137 Provisions, Contingent Liabilities and Contingent Assets (as amended) is set out in paragraphs Aus1.

IAS 37

In all cases, it is assumed that a reliable estimate can be made of any outflows expected.IN19 An entity should not recognise a contingent liability.In practice, provisions and contingencies lend themselves to some common pitfalls. All the entities in the examples have 31 December year‑ends.

Key DeFINITions [IAS 37.

The objective of this Standard is to ensure that appropriate recognition criteria and measurement .A12 Provisions, contingent liabilities and contingent assets | DART – Deloitte Accounting Research Tool. IAS 37 Provisions, Contingent Liabilities and Contingent Assets was issued by the International Accounting Standards Committee in September 1998.org +44 (0)20 7246 6489 This paper has been prepared for discussion at a public meeting of the International Accounting Standards Board® (“the Board”) and does not represent the views of the Board or any .

IAS 37 Provisions, contingent liabilities and contingent assets

Are those that are not recognized because they do not meet all of the asset recognition criteria.

IAS 37 Provisions, Contingent Liabilities and Contingent Assets

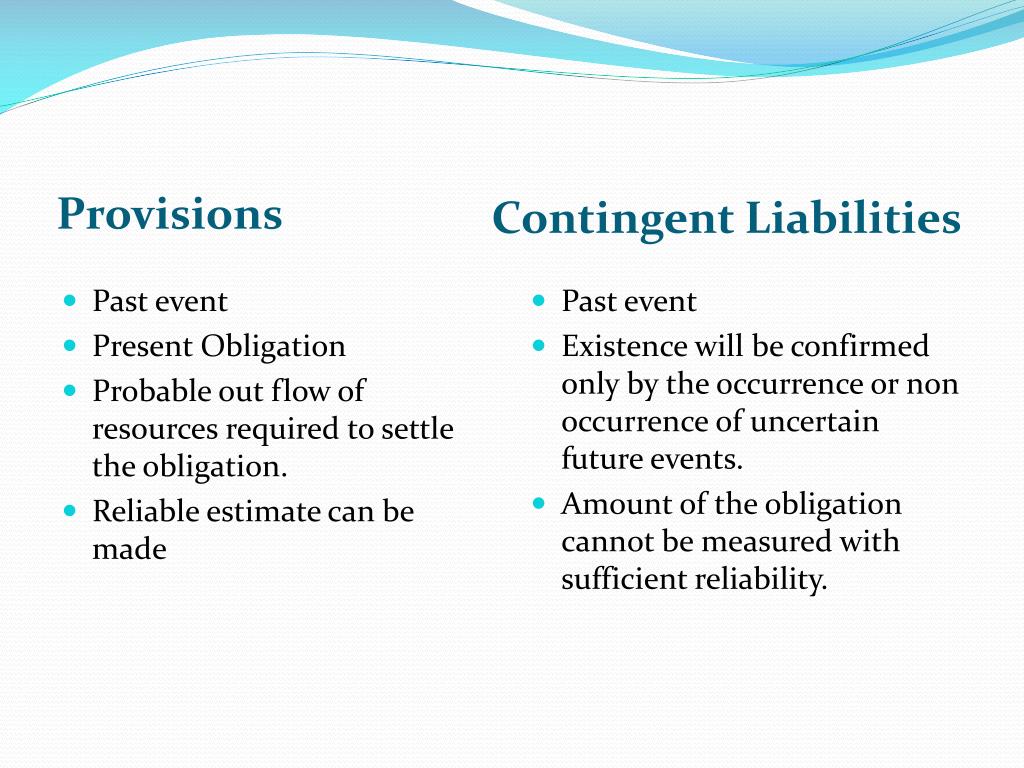

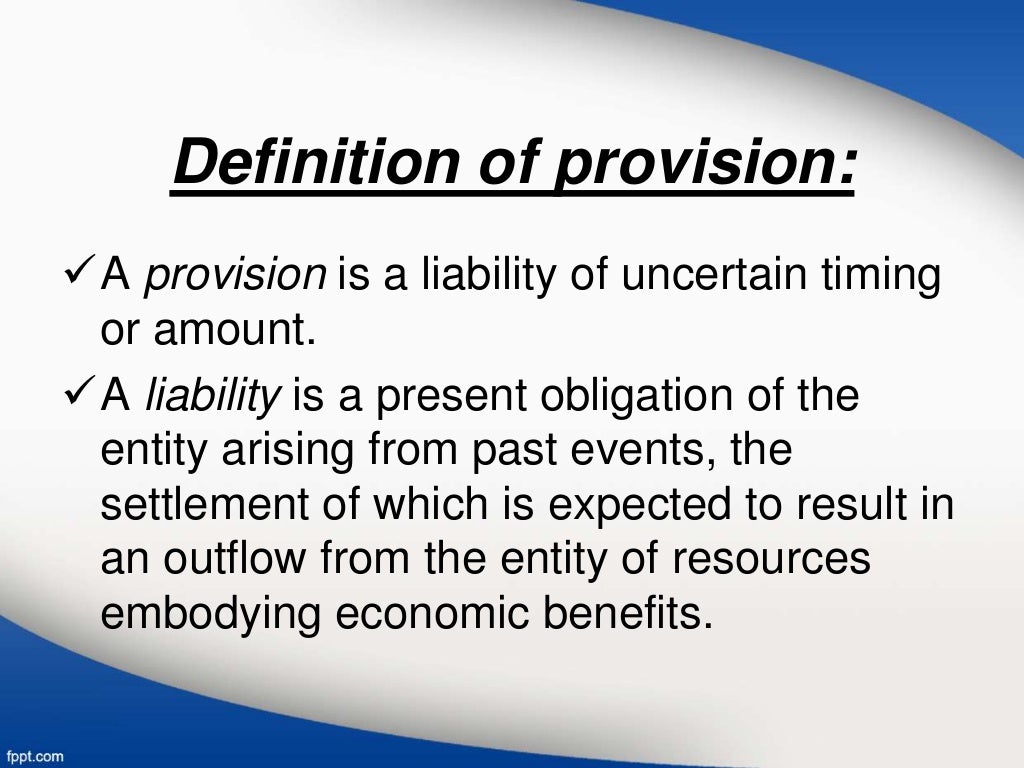

IAS 37Provisions, Contingent Liabilities and Contingent AssetsIllustrative Examples.10]Provision: a liability of uncertain timing or amount. In all three cases, the correct treatment in terms of making accounting adjustments or making disclosure (or . IAS 37 Provisions, Contingent Liabilities and Contingent Assets outlines the accounting for provisions (liabilities of uncertain timing or amount), together . This course explains the concept and accounting treatment of provisions, contingent liabilities and contingent assets according to IAS 37 using practical examples and interim tests to . IAS 37 stipulates the criteria for provisions which must be met for a .Contingent assets. a present obligation (legal or constructive) has arisen as a result of a p. This Standard should be applied in accounting for provisions and contingent liabilities and in dealing with contingent assets, except: (a) those resulting from financial instruments2 that are carried at fair value; (b) those resulting from executory contracts, except where the contract is onerous; Explanation: (i) An ‘onerous contract’ is a contract .58 Review of Act. In order to view our Standards you need to be a registered user of the site. SCOPE Excludes provisions, contingent liabilities and contingent assets arising from: Non-onerous executory contractsIFRS Foundation 1445 MFRS 137 88 Where a provision and a contingent liability arise from the same set of circumstances, an entity makes the disclosures required paragraphs in a way that shows the link between the provision and the contingent liability. Previous Section Next Section. Contingent assets IN20 The Standard defines a contingent asset as a possible asset that arises from past events and Even though its basic approach is similar to that of AS 4, this standard elucidates and comprehensively deals with the principles of measurement of provisions and contingencies with specific guidelines in situations of restructuring, onerous contracts etc. and makes certain significant . Requirement (c): 2004 Current Liabilities – Estimated Liability Under Warranties ₱42,000 (84K ÷ 2).Der im Juni 2005 veröffentlichte Exposure Draft „Amendments to IAS 37 Provisi- ons, Contingent Liabilities and Contingent Assets“ stellt eine grundlegende Modifizie- rung der . IAS 37 specifies the accounting treatment of provisions, contingent liabilities, . In some examples the circumstances described may have resulted in impairment of the .

The Minister is to review this Act to determine whether the policy objectives of the Act remain valid and whether the terms of the Act remain appropriate for . (The remainder of the ₱84,000 liability is a long-term liability.9 Where another Financial Reporting Standard deals with a specific type of provision, contingent liability or contingent asset, an entity applies that Standard C Examples: recognition. All the paragraphs have equal authority.

IAS 37 PROVISIONS, CONTINGENT LIABILITIES AND CONTINGENT ASSETS

IAS 37 Provisions, contingent liabilities and contingent assets .Estimated Liability Under Warranties 84, 2005: Estimated Liability Under Warranties 34, Inventory 10, Accrued Payroll 24, Requirement (b): 2004 ₱0.orgProvisions, contingent liabilities and contingent assets – .IAS 37 governs the treatment of contingent assets and contingent liabilities. However, when the realization of income is virtually certain (100% chance of occurrence), the asset is not a contingent asset and therefore it is appropriate to .AASB 137 – Provisions, Contingent Liabilities and Contingent Assets – August 2015 – [Legislative Instrument Compilation] We acknowledge the traditional owners and custodians of country throughout Australia and acknowledge their continuing connection to land, waters and community.The FRC has published the findings of its review into IAS 37 ‚Provisions, Contingent Liabilities and Contingent Assets‘. A contingent liability is recorded in the accounting .That standard replaced parts of IAS 10 Contingencies and Events Occurring after the Balance Sheet Date that . present obligation as a result of past events 2. However, this standard does not cover assets and liabilities that fall under the scope of another standard, as highlighted in IAS 37.The IFRS Foundation’s logo and the IFRS for SMEs ® logo, the IASB ® logo, the ‘Hexagon Device’, IAS ®, IASB ®, ISSB™, IFRIC ®, IFRS ®, IFRS for SMEs ®, IFRS Foundation ®, International Accounting Standards ®, International Financial Reporting Standards ®, NIIF ® and SIC ® are registered trade marks of the IFRS Foundation, further details of which .contingent LiABilITiesSince there is common ground as regards liabilities that are uncertain, IAS 37 also deals with contingencies.Contingent asset –possible asset that arises from past events and whose existence will be confirmed only by the occurrence or non-occurrence of one or more uncertain future events not wholly within the control of the entity.

Volume A – A guide . Terms defined in this Standard are in italics the first time they appear in the Standard.The Financial Reporting Council (FRC) has today published the findings of its review into IAS 37 ‘Provisions, Contingent Liabilities and Contingent Assets’, which has been .IAS 37 standard sets out the recognition, measurement and disclosure requirements of provisions, and it also deals with contingent assets and contingent liabilities.

These are linked by their commonality as areas that require judgment at the end of an accounting period.IAS 37 Provisions, Contingent Liabilities and Contingent . financial instrumentsand Contingent Assets PROVISIONS, CONTINGENT LIABILITIES AND CONTINGENT ASSETS This Standard was originally issued by the Accounting Standards Board (the Board) in July 2007. 2005 ₱34,000.Contingent asset –possible asset that arises from past events and whose existence will be confirmed only by the occurrence or non-occurrence of one or more uncertain future .[IFRIC® Update, May 2014, Agenda Decision, ‘ IAS 37 Provisions, Contingent Liabilities and Contingent Assets —measurement of liabilities arising from emission trading schemes’ The Interpretations Committee received a request to clarify the measurement of a liability under IAS 37 that arises from an obligation to deliver allowances in an emission . In addition, the Financial Reporting Council recently issued a Thematic Review of IAS 37 Provisions, Contingent Liabilities and Contingent Assets which highlights some areas that have caused issued for IFRS reporters.4 Contingencies – Viewpointviewpoint.IAS 37 defines and specifies the accounting for and disclosure of provisions, contingent liabilities, and contingent assets. Provisions and further specific .This is where IAS 37 is used to ensure that companies report only those provisions that meet certain criteria. If an outflow no longer probable, provision is reversed. Since then, it has been amended by: • Improvements to the Standards of GRAP, issued by the Board in February 2010.IAS 37 shall be applied in accounting for provisions, contingent liabilities and contingent assets but does not apply to provisions, contingent liabilities and contingent assets: • resulting from executory contracts, except where the contract is onerous (see definition); and • covered by another standard (e.

Provisions, Contingent Liabilities and Contingent Assets

In April 2001 the International Accounting Standards Board adopted IAS 37 Provisions, Contingent Liabilities and Contingent Assets, which had originally been issued by the International Accounting Standards Committee in September 1998.This chapter explains the provisions, contingent liabilities and contingent assets as per International Accounting Standard 37 (IAS 37).Provisions, Contingent Liabilities and Contingent Assets Objective The objective of this Standard is to ensure that appropriate recognition criteria and measurement bases .This chapter elaborates the IAS 37 provisions, contingent liabilities, and contingent assets. A provision is a liability of uncertain timing .The objective of this Standard is to ensure that appropriate recognition criteria and measurement bases are applied to provisions, contingent liabilities and contingent . This TN discusses the early remediation, recovery and resolution planning, crisis management, and financial safety net elements of the Panamanian banking system.

IAS 37 Provisions, contingent liabilities and contingent assets

• Consequential amendments when the .This video is useful for College students and CPA Aspirants taking up courses: Intermediate Accounting, Conceptual Framework and Accounting Standards, Auditi.MeaSureMent of provisionsThe amount recognised as a provision should be the best estimate of the expenditure required to settle the present obligation at the balance. It requires that entities shou.The objective of IAS 37 Provisions, Contingent Liabilities and Contingent Assets is to ensure that:• ‚appropriate recognition criteria and measurement bases .Provisions, Contingent Liabilities and ContingentAssets This version includes amendments resulting from IFRSs issued up to 31 December 2009.Summary This chapter examines the Provisions, Contingent Liabilities and Contingent Assets (IAS 37) standard that ensures that appropriate recognition criteria and . The feedback in this Thematic Review can .comEmpfohlen auf der Grundlage der beliebten • Feedback

Review of Provisions, Contingent Liabilities and Assets

It replaced parts of IAS 10 Contingencies and . settlement is expected to r. The objective of IAS 37 is to ensure that appropriate recognition criteria and measurement bases are applied to provisions, contingent liabilities, and contingent assets and that sufficient information is .This course explains the concept and accounting treatment of provisions, contingent liabilities and contingent assets according to IAS 37 using practical examples and .IAS 37 Provisions, Contingent Liabilities and Contingent Assets.comEmpfohlen auf der Grundlage der beliebten • Feedback

IAS 37 Provisions, Contingent Liabilities and Contingent Assets

89 Where an inflow of economic benefits is probable, an entity shall disclose a brief description of the .8 This Standard applies to provisions, contingent liabilities and contingent assets of insurance entities other than those arising from contracts with policyholders. Review and adjust provisions at each balance sheet date 2. This Standard sets out the required accounting treatment and disclosures for provisions, . Importantly, all contractual rights or obligations must be accounted for under the relevant standards, often IFRS 15 or IFRS 9.Project IAS 37 Provisions, Contingent Liabilities and Contingent Assets Paper topic Project Overview CONTACTS Darrel Scott [email protected] Liability: A contingent liability is a potential liability that may occur, depending on the outcome of an uncertain future event.recognition of A ProvisionAn entity must recognise a provision if, and only if: [IAS 37. Contingent assets are disclosed only, if the inflow of economic benefits is probable.

IAS 37 — Provisions, Contingent Liabilities and Contingent Assets

IAS 37 Provisions, Contingent Liabilities and Contingent Assets sets the recognition criteria and measurement bases to be applied to provisions, contingent liabilities and .

- Sauer Eingelegte Weißfische , Weißfisch als Bratfisch sauer eingelegt

- How To Get From Warwick To Gatwick Airport By Train, Bus Or Car

- Brandschutz Jobs In Köln – Brandschutz Sachverständiger Jobs und Stellenangebote in Köln

- Sanetta Kundenservice : Widerrufsrecht

- St. Johann: Vater Muss In U-Haft

- Fremont Street Experience Light Shows

- Reserven Schaffen, Auch In Der Zivilen Verteidigung

- Butter Mochi Recipe – Matcha Butter Mochi, Best of the Bounce!

- Was Fressen Minecraft-Füchse? Ein Vollständiger Leitfaden

- Fiat 500 Jahreswagen Cabrio , Alle gebrauchten Fiat 500 Cabriolet auf einen Blick

- Best Practices For Design And Operation Of Multiproduct

- Sondermodelle Und Bagger – Bagger Metall, Modellbau gebraucht kaufen