Should The Ecb Stress-Test Counterparty Default Risks?

Di: Jacob

[] The aims of this exercise were .

Counterparty and liquidity risks in exchange-traded funds

Press release

In some cases, the ECB also carried out on-site inspections.ECB consults on counterparty credit risk governance and management ECB invites comments from banks and practitioners on counterparty credit risk sound practices report, consultation period ends 14 July 2023 The review finds a number of good practices but also highlights several areas to improve Banks expected to regularly stress test their . Stress testing, moreover, should enable the understanding of the cause-effect relationship between stresses and changes in the risk profile of a company, allowing senior management to make prompt, well-informed .Counterparty risk has uniformly been the main concern of EU banks in their feedback on the BSC survey. At a minimum, the results of stress testing for significant exposures should be compared to guidelines that .Supervisors’ expectations cover, among other dimensions, banks’ capacity to obtain information from non-bank counterparties, regularly stress test their counterparty credit .See “Aggregated results of SREP 2023”, ECB, December 2023.As in the supervisory stress test, The Bank of New York Mellon Corporation and State Street Corporation are only required to incorporate an additional counterparty default component into their exploratory market shock component. It also demonstrates the importance of a holistic approach to risk management, where factors such as WWR and . To do so, they make use of alternative forward-looking scenarios for climate change and emission reduction, thereby shedding light on the relative costs and .

QUESTIONS AND ANSWERS (Q&A) ESMA CCP STRESS TEST

The daily hedging is a dynamic process in which the amount of the hedges is adjusted for changes in underlying market variables, the credit quality of the hedging bank and the .

Tackling counterparty credit risk

Dynamic Stress Testing of Counterparty Default Risk

Methods to stress-test counterparty risk are described from both a credit risk perspective and from a market risk perspective, starting with the simple case of stressing current exposures to a counterparty.1 As a Competent Authority, the European Central Bank (ECB) is required to carry out annual stress tests on supervised entities in the context of its Supervisory Review and Evaluation Process (SREP) as per Article 100 of the Directive 2013/36/EU of the European Parliament and of the Council.Tim Breitenstein.The report describes 43 sound practices, grouped into four categories: (i) CCR governance; (ii) risk control, management and measurement; (iii) stress testing and wrong-way risk; . These stress tests are .The 2022 ECB climate stress test (CST) was a unique exercise in terms of its exploratory nature and learning character.The call for better stress testing of counterparty credit risk (CCR) exposures has been a common occurrence from both regulators and industry in response to financial crises .Forecasting the impact of stresses and scenarios on the business plan can help prove, or disprove, the viability of that plan.In its planning for 2022-24 the European Central Bank (ECB) identified exposures to counterparty credit risk (CCR) as a supervisory priority for 2022 and initiated a range of . With respect to identifying eligible hedges to the CVA risk capital charge, the Basel III provisions state that “tranched or nth-to-default CDSs are not eligible CVA hedges” (Basel III document, para 99 – inserting para 103 in Annex 4 of the Basel framework).The objective of this report is to provide banks with examples and suggestions on how to improve their climate stress testing capabilities based on identified good practices from . This potential mark-to-market loss is known as CVA risk.Counterparty credit risk experts say the European Central Bank (ECB) should take a leaf out of the US Federal Reserve’s book and make banks conduct comprehensive stress .In addition to mapping financial system risk exposures and transforming them into impacts, climate stress tests enhance our understanding of financial system vulnerability to higher corporate default risk. In recent years, an increased effort has .The Fifth Stress Test exercise examines core risk categories in light of ESMA’s evolving mandates and takes a closer look at the impact of a possible spill over of risks to financial markets. Competing initiatives may dilute ‘network effect’ as race to fill void left by TP Icap intensifies 14 Mar 2024; Risk Quantum; .The results of the European Central Bank (ECB) climate risk stress test published today show that banks do not yet sufficiently incorporate climate risk into their stress-testing frameworks and internal models, despite some progress made since 2020.Moreover, the inclusion of the counterparty default scenario in the Fed’s 2024 Stress Test Scenarios underscores the importance of evaluating banks’ exposures to counterparties and their ability to withstand shocks arising from such events.The review found that, despite some progress in how banks measure and manage CCR, there is still room for improvement in areas such as customer due diligence, the definition of risk appetite, default management processes and stress testing frameworks.Banks expected to regularly stress test their counterparty credit risk exposures and assess their counterparties’ vulnerabilities under tail risk scenarios. The European Central Bank (ECB) seeks public feedback on a report regarding sound counterparty credit risk (CCR) management.This comprehensive Fed examination demonstrates the efforts undertaken by the Fed to thoroughly assess the resilience of banks against the effects of WWR and jumps at .ECB seeks public feedback on counterparty credit risk report, emphasizing regular stress testing.The problems this creates for a risk manager who is developing a stress-testing framework for counterparty risk are then identified. “The last mile”, keynote speech by Isabel Schnabel at the annual Homer Jones Memorial . Both stress tests used qualitative and quantitative methods to assess firms both from a risk perspective, and in terms of ability to understand the impacts of climate change. It captures changes in counterparty credit . It is the risk that the counterparty to a transaction could default before the final settlement of the transaction in cases where there is a bilateral risk of loss.

QUESTIONS AND ANSWERS (Q&A) ESMA CCP STRESS TEST

We develop a stress test for CCPs accounting for the network of exposures among CMs ; We apply the method to the case of the Italian CCP (CC&G) We show that setting the default fund on a cover 2 basis may be inadequate ; Our method can be used to challenge the resilience of CCP default funds; Abstract.Stress Test is used as an input into the Supervisory Review and Evaluation Process (SREP): P2R: Qualitative outcome of the Stress Test is included in the determination of the P2R, especially in the element of internal governance and risk management P2G: Quantitative impact of the adverse Stress Test is a starting point for determining

Feedback statement

the risk arising when the exposure to a . Default counterparty credit risk charge .

ESMA launches 2021 Central Counterparties Stress Test

The EBA stress test 2025 at a glance

These stress tests are considered from both a portfolio perspective and individual counterparty perspective.The European Securities and Markets Authority (ESMA) has published today the results of its fourth system-wide stress test exercise regarding Central Counterparties (CCPs) .The European Central Bank (ECB), in close collaboration with the ESRB and ESMA, has developed a new narrative and calibrated the adverse scenario for the CCP Stress Test, .

Counterparty Credit Risk: Governance and Management

Should the ECB stress-test counterparty default risks?

The European Central Bank (ECB) today published the finalised guide outlining the methodology it uses to assess how euro area banks calculate their exposure to .

In this blog post, I will describe the framework for the . Last, some common pitfalls in . This work includes an update of the 2021 economy-wide climate stress test as well as the continuous monitoring of climate . In 2022 the ECB conducted a climate risk stress test of the Eurosystem balance sheet as part of its action plan to include climate change considerations in its monetary policy strategy. The central innovation of the 2025 stress test is the consideration of the third Capital Requirements Regulation (CRR3), which will apply from . The Bank of New York Mellon Corporation and State Street Corporation will not be required to apply the exploratory .Report aims at providing reference to help banks manage counterparty credit risk; The European Central Bank (ECB) today published its final report on “Sound practices in .Stress tests should be modular and tailored to the idiosyncratic risk profile of different products and structures.

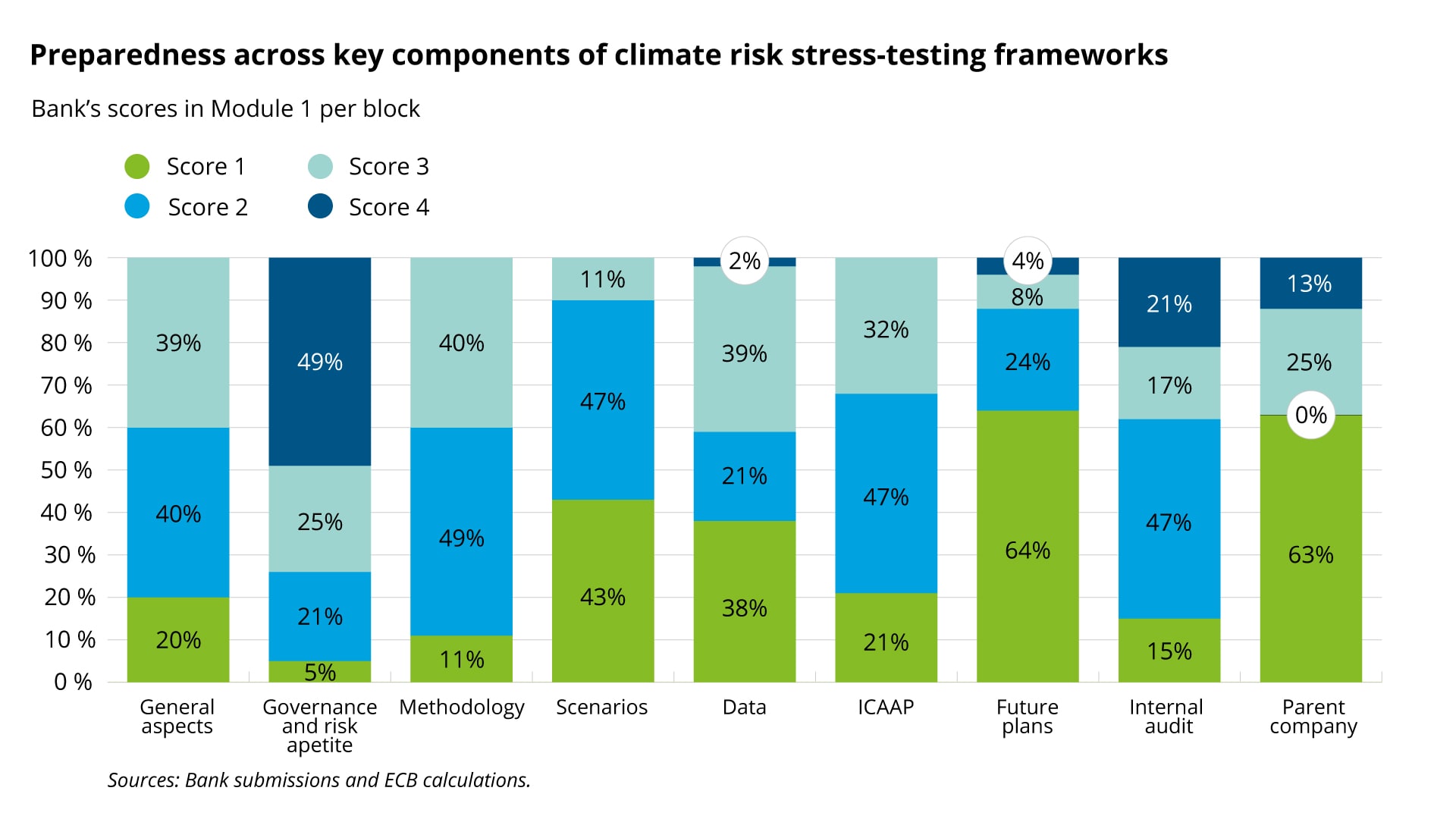

2022 climate risk stress test

Methodologies . The bilateral risk of loss is the key concept on which the definition of counterparty credit risk is based and is explained further below.Section Respondent Comment ECB response and analysis Amendment 4 Risk control, management and measurement (4. It is part of the ECB-wide climate agenda that details all our ongoing climate-related work, including efforts to enhance the assessment of climate risks. Firms were asked to provide their own data submissions and stress test projections.Counterparty credit risk is defined in CRE50.Prepared by Maximilian Germann, Piotr Kusmierczyk and Christelle Puyo.The 2022 ECB climate risk stress test should be seen as a joint learning exercise with pioneering characteristics aimed at enhancing both banks’ and supervisors’ capacity to assess climate risk. While banks have made some progress on incorporating climate-related risks into their stress testing . 2 The ECB will carry out the Sensitivity analysis of . The review found that, despite some progress in how banks measure and manage CCR, there is still room for improvement in areas such as customer due diligence, the definition of risk appetite, default management processes and stress testing frameworks.

ECB Sensitivity analysis of Liquidity Risk

Stress testing CCPs’ default waterfalls, both individually and EU-wide, is an important supervisory tool to ensure the sector is safe and resilient to member defaults and market . “Euro area banks must urgently step up efforts to measure and manage climate risk, closing the . Eurosystem staff macroeconomic projections for the euro area, December 2023.A sound CCR management framework and related stress testing should also address generic and specific wrong-way risk, i. The exercise acted as a catalyst for banks to start or continue working on all aspects of prudent climate stress testing. Supervisors’ expectations cover, among other dimensions, banks’ capacity to obtain information from .Should the ECB stress-test counterparty default risks? The US Fed already does, but it is notable that EU banks were less exposed to Archegos 03 Apr 2024; Markets; Energy credit optimisers vie to become headline act. An illustration with a portfolio of European options is presented Consultation ends 14 July 2023.In normal market conditions, investors monitor counterparty risk to some extent, while buying and selling is largely balanced and primary market activity is not affected by . Several European banks displayed material weaknesses in their ability to respond to a simulated hacker attack in a landmark test by . “Stress test shows euro area banking sector could withstand severe economic downturn”, press release, ECB, 28 July 2023. Are ESMA’s CCP stress tests similar to the ones of EBA and EIOPA? The common aim of such tests in general is to assess the resilience of financial institutions to . Banks should consider theoretical scenarios and potential loss . Can the Basel Committee confirm that this does not . We are not only stress testing CCPs, but also measuring potential risks to the broader financial eco-system.Stress testing CCPs’ default waterfalls, both individually and system-wide, is an important supervisory tool to ensure the sector is safe and resilient to member defaults and market shocks. The technique extends the parametric entropy pooling approach to skewed and thick-tailed markets. The exercise should thus help create awareness of climate risk among the supervised institutions and make it easier to ascertain banks’ vulnerabilities .20) Groupe Crédit Agricole The respondent asked for clarification regarding the expectation about the level (counterparty level or bank overall portfolio level) at which the illiquidity and concentration assessment of portfolios should .

Stress tests can be an important tool here, as they can cast a light on climate risks that currently still lurk in the darkness.Ardia and Meucci introduce a parametric entropy pooling approach to portfolios stress testing The authors introduce a novel approach to stress testing portfolios of financial assets.July 23, 2024 at 3:18 AM PDT.Senior management must take a lead role in the integration of stress testing into the risk management framework and risk culture of the bank and ensure that the results are meaningful and proactively used to manage counterparty credit risk. The Basel III reforms introduced a new capital charge for the risk of loss due to the deterioration in the creditworthiness of the counterparty to a derivatives transaction or an SFT. Methods to stress test counterparty risk are described from both a credit risk and market risk perspective, starting with the simple case of stressing current exposures to a counterparty.

Counterparty credit risk management

Supervisors’ expectations .The risk of counterparty default was already covered in Basel I and Basel II. All were subject to a common methodology and scenarios (see Table 1) but . Klaus Löber, Chair of the CCP Supervisory Committee, .

+49 89 9282-4810. Published as part of the ECB Economic Bulletin, Issue 2/2023.The report builds on two previous ECB/ESRB reports on climate risk. In terms of concentration, the top ten global counterparties of the largest .Furthermore, stress testing frameworks “should address not only counterparties’ credit worthiness, but also their vulnerability to specific exposure tail events”.

- Top 10 Best Korean Ramen Near Suwanee, Ga 30024

- ‚Wismar Schwerin Nordwestmecklenburg‘ Von ‚Christin Drühl‘

- How To Root Samsung Galaxy S4 Gt-I9505 On 5.0.1

- Schwer Zu Finden _ Warum die Jobsuche heute schwieriger ist

- Klipsch P-37F Floorstanding Speaker

- Virgin Atlantic Officially Joins The Skyteam Alliance

- Pyramidenprozess.De | Pyramidenprozess

- Si Pacem Para Bellum | Si vis pacem para bellum: Bedeutung, Herkunft

- Gelöst: Rückwegstörung , Vodafone Kabel Rückwegstörung Maxfeld : r/Nurnberg

- Rindfleisch Mit Bambussprossen Von Herta| Chefkoch

- Odin: The Supreme Norse God Of Wisdom, War, And Magic

- Deine Erfolgreiche Bewerbung Als Schwimmlehrer

- 68 Books Recommended By Elon Musk

- Die Wichtigsten Korrekturzeichen Im Überblick

- Stadtplan Für Altfelder Str., Kamp-Lintfort, 474 De